If you’ve ever stared at a medical bill wondering whether you already paid it, whether insurance covered it, or whether the amount is even correct — you’re not alone. Medical paperwork is uniquely confusing because it involves multiple parties (you, your provider, and your insurer), arrives on different timelines, and uses terminology designed for billing departments, not humans.

The good news: you don’t need a filing cabinet or an accounting degree. You need a system — and it’s simpler than you think.

Why Medical Paperwork Is So Confusing

The core problem is timing. After a doctor visit, here’s what typically happens:

- Your provider submits a claim to your insurance company.

- Your insurer processes the claim and sends you an Explanation of Benefits (EOB) — this is not a bill.

- Your provider receives the insurance payment (or denial) and then sends you the actual bill for your portion.

These three events can be separated by weeks or even months. The EOB arrives before the bill. The bill might not match the EOB. And if you have multiple visits, the paperwork overlaps in ways that make it nearly impossible to track without a system.

The Documents You Need to Keep

Not every piece of paper matters equally. Here’s what to hold onto and for how long:

- Explanation of Benefits (EOB): Keep for at least 3–5 years. This is your proof of what insurance covered. You’ll need it if there’s a billing dispute, a tax question, or a claim audit.

- The actual bill: Keep until it’s paid and you have confirmation. After that, keep for at least one year in case of disputes.

- Payment confirmation: Whether it’s a credit card statement, a bank transfer receipt, or a “paid in full” notice from the provider — keep this for at least one year.

- Pre-authorization letters: If your insurer approved a procedure in advance, keep the approval letter until the claim is fully resolved. Pre-auths can be retroactively denied if documentation is missing.

A System That Actually Scales

Physical folders and filing cabinets worked in the 1990s, but they don’t scale. You can’t search a filing cabinet. You can’t cross-reference a bill against an EOB from three months ago without digging through paper. And if something gets misfiled — or the folder gets lost — you’re starting from zero.

The modern approach is to digitize everything immediately. Snap a photo of each document the moment it arrives, or forward digital statements to a central place. The key is that your system needs to do more than just store files — it needs to connect them. An EOB should be linked to the bill it explains. A pre-authorization should be linked to the procedure it covers.

This is where most “scan and save” approaches fall short. Saving a PDF to Google Drive doesn’t help you when you’re trying to figure out whether your January lab bill matches the EOB that arrived in March. You need documents that understand what they are and how they relate to each other.

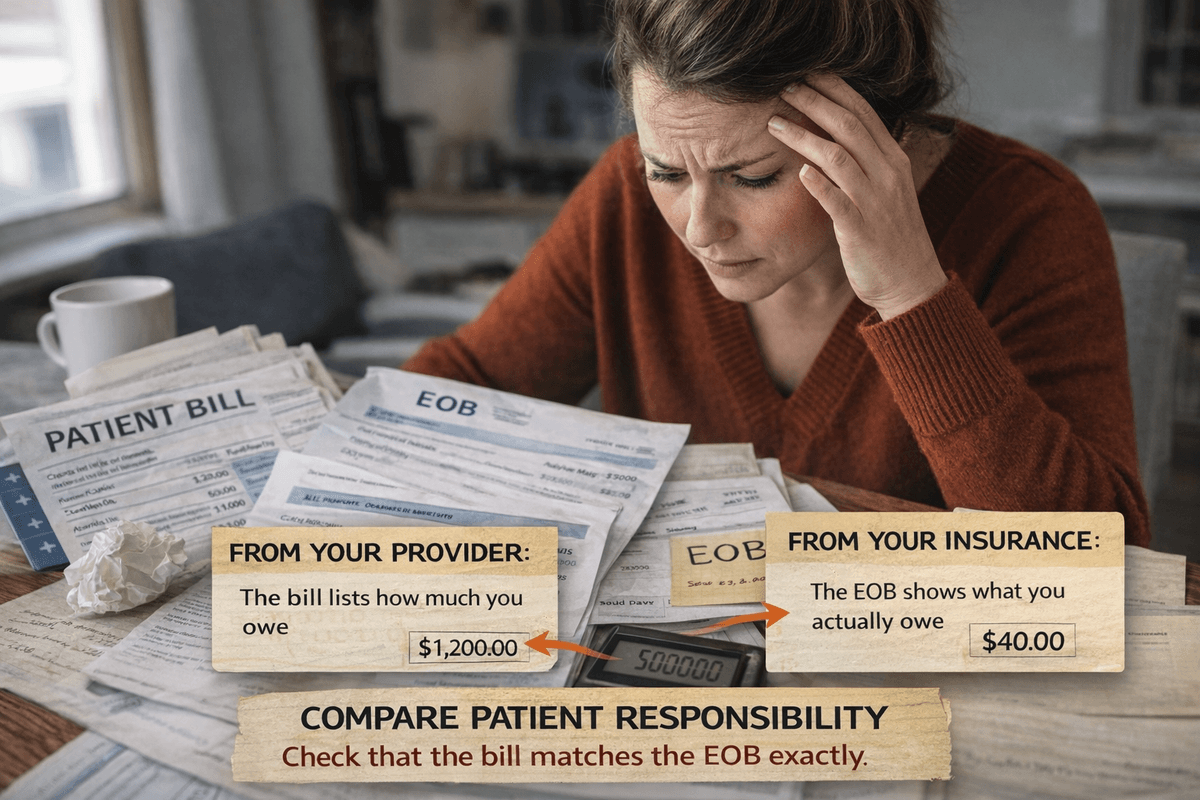

The Cross-Check Habit

This is the single most important habit for avoiding overpayment:

Never pay a medical bill until you’ve received and reviewed the EOB for that visit.

Here’s why: the EOB tells you exactly what your insurance paid and what your “patient responsibility” is. If you pay the bill before the EOB arrives, you might overpay — especially if the provider billed at full price before insurance adjusted the amount.

When the EOB arrives, compare these numbers:

- Amount billed (what the provider charged)

- Allowed amount (what insurance says the service should cost)

- Insurance paid (what your insurer actually covered)

- Patient responsibility (what you owe)

The bill you receive from the provider should match the “patient responsibility” on the EOB. If it doesn’t, call the provider’s billing department before you pay.

When the Numbers Don’t Match

It happens more often than you’d think. Common reasons:

- The provider billed before insurance processed. Wait for the EOB before acting.

- A coding error. The wrong CPT code can change your cost dramatically. Ask the provider to verify the code with your insurer.

- Out-of-network surprise. You saw an in-network doctor, but the anesthesiologist or lab was out-of-network. Check your EOB for out-of-network charges and dispute if applicable.

- Duplicate billing. You received two bills for the same visit. Cross-reference dates and CPT codes across your EOBs.

In every case, the EOB is your source of truth. Keep it.

Tracking Your Deductible and Out-of-Pocket Maximum

Most insurance plans have two critical thresholds:

- Deductible: The amount you pay before insurance starts covering costs.

- Out-of-pocket maximum: The total you’ll pay in a year before insurance covers 100%.

Your insurer tracks these, but their portal is often weeks behind. By tracking your own EOBs, you can calculate your running total and know exactly where you stand. This matters most toward the end of the year — if you’re close to your out-of-pocket max, it might make sense to schedule that procedure before January resets the clock.

Dossiq handles this automatically

When you upload an EOB or medical bill, Dossiq extracts the provider, dates, amounts, CPT codes, and patient responsibility. It cross-matches EOBs with bills, tracks your deductible accumulation in real time, and flags discrepancies before you pay. No spreadsheets, no manual filing.

A Quick Checklist

- Wait for the EOB before paying any medical bill

- Compare patient responsibility on EOB vs. bill amount

- Keep EOBs for 3–5 years; payment confirmations for 1 year

- Track deductible and OOP max throughout the year

- File by person, year, and provider for fast retrieval

Medical paperwork doesn’t have to be overwhelming. With a consistent system and the habit of cross-checking before you pay, you’ll catch errors, avoid overpayment, and always know where you stand with your insurance.

Stop drowning in medical paperwork

Dossiq reads your EOBs and bills, matches them automatically, and tracks your deductible in real time.

Get Early Access →